🇺🇸 Sonoco: Packaging Powerhouse with Sustainable Growth Momentum

Stock Idea #84

Hello! Welcome to this week’s stock idea, I am super late, I am sorry. Today’s focus is on Sonoco Products, a stalwart in industrial packaging with a robust operational profile and an attractive valuation. They have 100 years of expertise in the field!

Let’s dive into why this company stands out.

Company Presentation

Sonoco Products is a global leader in industrial packaging, with more than a century of experience providing innovative packaging solutions across diverse sectors including consumer goods, healthcare, and industrial applications. With operations spanning over 30 countries and a workforce exceeding 20,000 employees, Sonoco leads through a commitment to sustainability and advanced manufacturing technologies.

Its recent acquisition of Eviosys, a leader in metal packaging in Europe, further strengthens its market presence and broadens its product capabilities.

Business and Financial Highlights

Sonoco delivers integrated packaging solutions combining advanced materials, sustainable design, and automation technology. The company generated strong financial results in 2025, marked by a 37% increase in EBITDA to $386 million in Q3, supported by high demand and operational efficiency improvements. Its free cash flow generation remains consistent, allowing a healthy dividend yield of approximately 4.5%. Sonoco’s balance sheet, while impacted by recent acquisitions, reflects strategic investments that enable long-term growth and competitive positioning in evolving markets such as eco-friendly packaging.

Market Opportunity & Why Now

The industrial packaging market is undergoing transformation driven by: sustainability mandates, consumer demand for eco-conscious products, and digital integration in supply chains and I believe Sonoco’s portfolio aligns well with these trends, with for instance smart investments in recyclable materials and digital printing technologies. Growing global e-commerce and logistics needs further enhance the demand for Sonoco’s packaging solutions. The backlog from recent contracts and increased market share from Eviosys acquisition signals potential for continued revenue growth.

Moat Assets Strength

Obviously Sonoco’s competitive edge lies in its expertise created on the long run and so, the diversified product portfolio they get with time; proprietary packaging technologies, and strong customer relationships built over decades. Its focus on sustainability enhances switching costs as clients seek certified, eco-friendly solutions.

Heavy investment in R&D (around $100 million annually) fuels ongoing innovation and shows they anticipate market growth and opportunity. While the packaging industry has competitive players, Sonoco’s scale, product quality, and integrated services create considerable barriers to entry.

Moat Strength: 7/10

Pricing Power & Financial Momentum

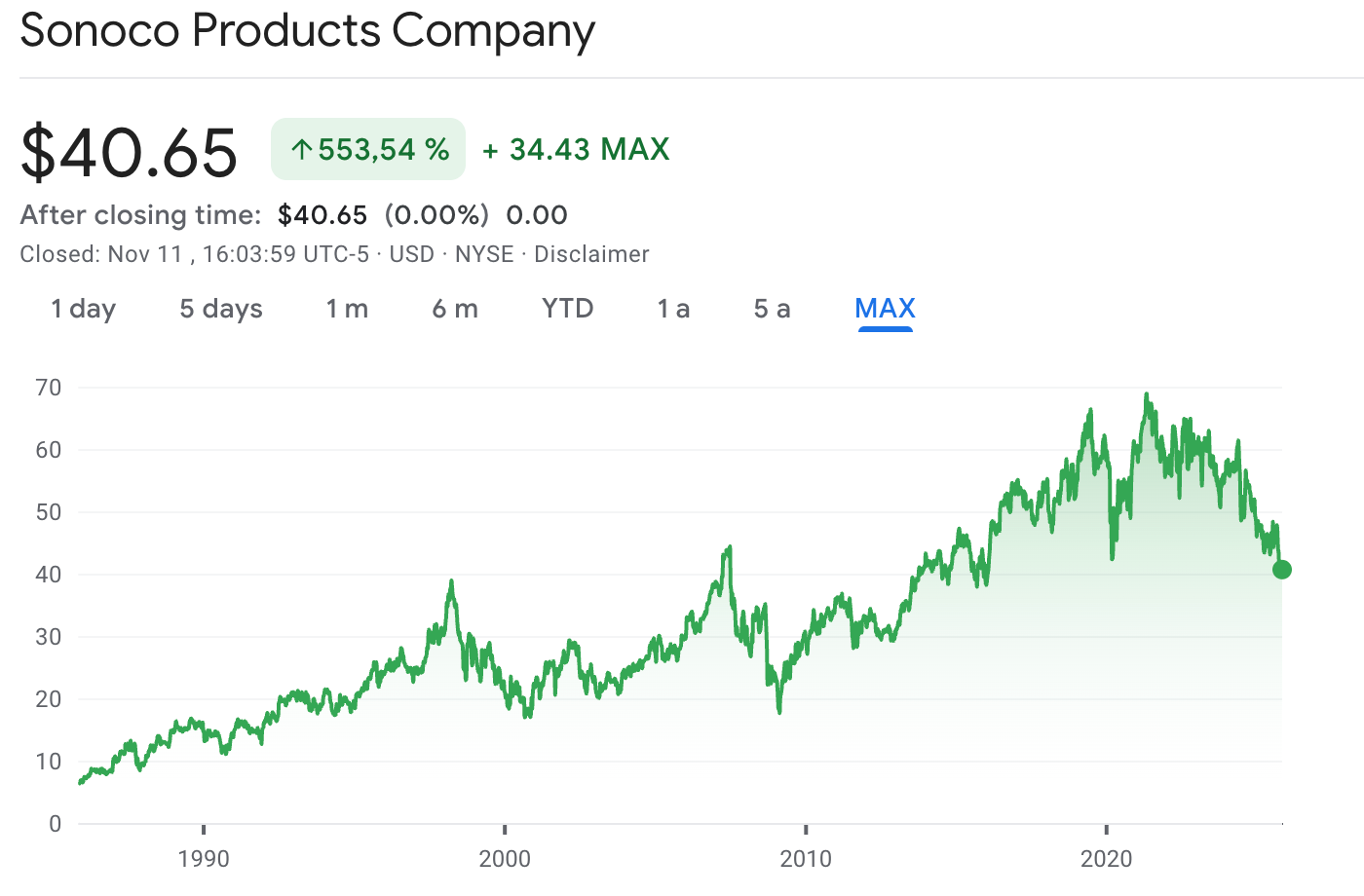

Sonoco benefits from pricing power backed by its position, its innovation and sustainability credentials, enabling margin improvements despite commodity input inflation…

Its EBITDA margin improved significantly in 2025, with solid operational leverage (please see image above). Recurring revenue streams from long-term supply agreements support cash flow stability.

The company’s consistent free cash flow generation supports a reliable dividend policy, currently yielding close to 4.5%, with management targeting further margin expansion and deleveraging post-acquisition.

Pricing Power & Financial Momentum: 8/10

Market Neglect

Although well-known in packaging circles, Sonoco remains relatively underfollowed by broader institutional investors compared to tech or consumer sector stocks. Its listing on the NYSE and diversified business lines lead to moderate visibility. This creates an opportunity for patient investors to capitalize on growth ahead of widespread recognition, especially as sustainability transitions accelerate across industries.

Market Neglect: 5/10

Insider Alignment

Management holds a meaningful equity stake in Sonoco Products, with insiders owning approximately 8.11% of the company’s total shares as of October 2025, representing around 8 million shares out of nearly 98.6 million outstanding shares. The CEO, Robert Howard Coker, personally holds about 0.5% of the shares and has actively purchased shares worth over $1.7 million in 2025, demonstrating strong alignment with shareholder interests, or… that he knows something we don’t.

Institutional investors own about 83% of Sonoco’s shares, with major stakeholders including BlackRock holding around 11%. Other large institutions hold between 4.5% and 11% each, while the general public owns roughly 16%.

This distribution reflects a balanced governance structure, with significant insider involvement ensuring a good alignment of interests and disciplined capital allocation. Insider transactions in recent years have been net positive, reinforcing confidence in the company’s strategic direction and long-term value creation.

Insider Alignment: 7/10

Risk Asymmetry & Risks That Lurk

Key risks I identified for this big player include exposure to raw material price volatility of coruse, global supply chain disruptions, and economic cycles affecting packaging demand. The integration of heavy acquisitions like Eviosys temporarily pressures cash flow and debt metrics. Competition in packaging materials, especially from emerging technologies, poses big risk. However, strong operational cash flow, diversification, and management capability mitigate downside risks. Future upside depends on successful synergy realization and expanded eco-friendly product adoption. And that’s the way they seem to go to.

Risk Asymmetry: 6/10

Conclusion

Sonoco Products exemplifies a mature industrial packaging company positioned for profitable growth through strategic acquisitions, innovation in sustainable materials, and solid free cash flow generation. With a strong moat, pricing power, and moderate market neglect, it offers an attractive risk-reward profile for investors seeking exposure to long-term trends in packaging and sustainability.

Moat Strength: 7/10

Pricing Power & Financial Momentum: 8/10

Market Neglect: 6/10

Insider Alignment: 7/10

Risk Asymmetry: 6/10

➡️ Total Hidden Score: 33/50

🔙 One Year Ago in HMG: Lifco

🇸🇪 Lifco: The Serial Acquirer

At first glance, when I saw that Lifco seemed to do a bit of everything, I thought, “Uh-oh, trying to be good at everything often means being good at nothing.” But then, I realized they actually manage their business exceptionally well—very, very well.

Lifco’s activity over the past year (2024-2025) has been marked by steady growth and a continuing strategic acquisition spree. According to their interim report for January-September 2025, Lifco reported a 9.0% increase in net sales to SEK 20.7 billion, consisting of 4.3% organic growth and 7.4% contributed by acquisitions. The company consolidated 13 new businesses during this period, reinforcing its market positions across dental, demolition & tools, and systems solutions sectors.

This analysis is for informational purposes only and does not constitute financial advice or investment recommendations. Investing in financial markets involves risks, including the risk of loss of capital. Always do your own research or speak with a qualified advisor.

Be careful with using Google financials. The income for SON includes the $625M capital gain for the TFP divestiture. I'm not sure the dividend is sustainable. Capex was roughly in line with operating cash flow last quarter. I hope Enviosys can pick up the slack.